The UK business community stands side-by-side with the government and the action it is taking in opposing Russian aggression and supporting Ukraine and its people. The CBI has already begun working closely with members regarding Ukraine, the impact of Russian sanctions and the information flow with government. This brief note summarises some initial analysis on the impact on the UK economy via four main channels, but we would also welcome your thoughts/insights (please email us at [email protected]).

Energy and other commodities

At a macro level, higher energy prices are the most immediate impact on the UK economy. Russia is the third largest oil exporter in the world. It supplies around 5% of the UK’s total natural gas imports, but around 40% of the EU’s gas imports. Just the threat of disruption to energy supplies has sent oil and wholesale gas prices sharply higher, with the price of a barrel of Brent Crude hitting 8-year highs of just over $100, and UK gas futures increasing by over 40%. Though energy has so far been spared sanctions, additional hurdles to financial payments to Russian entities increase the possibility of less Russian oil and gas reaching the market. This is likely to keep global energy prices higher for longer, with analysts’ oil price forecasts for the coming months in a range of $110-120 p/b. Disruption to physical supply—potentially an act of Russian retaliation—is an upside risk.

The same is true of other global commodity markets, which are already tight owing to the disruptions inflicted by COVID-19, so prices are highly responsive to even the smallest supply shocks. Russia and Ukraine are major exporters of non-energy commodities, particularly industrial metals and foodstuffs, as well fertilisers. There are reports that the closure of Ukrainian ports and rail is disrupting exports of key commodities (with 90% of Ukrainian grain exports transported by sea, for example). Higher global prices will ripple through to end users, adding to existing cost pressures for firms in a range of sectors, particularly food & drink, chemicals, metals, automotive, aerospace, technology and construction.

Direct trade and financial links

From a macroeconomic perspective, disruption to direct trade with Russia and Ukraine poses less of a risk: the two countries account for less than 1% of UK exports and around 1.5% of imports, with foreign investment and incomes flows also relatively small. However, exposure varies greatly for individual businesses, many of which have already suspended shipments to Russia, are considering alternative suppliers and whether to divest of their Russian operations altogether, in some cases at a considerable financial cost.

Confidence and the policy response

A fourth important transmission channel is via the hit to confidence and the broader tightening financial market conditions which, all else equal, will tend to weaken growth. This adds to the dilemma facing the Bank of England, which must weigh up the impact of higher energy prices on domestic inflation against corresponding hits to demand. While rising uncertainty might normally encourage the Bank to adopt a “wait-and-see” approach, existing concerns around near-term inflation expectations and wage-price dynamics suggest that the Bank will press ahead with a series of small interest rate rises this year.

Key statistics:

- Employment rate (Sep 2021 – Nov 2021): 75.5%

- Unemployment (Sep 2021 – Nov 2021): 4.1%

- Productivity growth (Output per hour, Q3 2021

vs 2019 pre-pandemic levels): +1.1% - Real wage growth (Sep 2021 – Nov 2021 on a year ago, excl. bonuses): 0.0%

- CBI growth indicator: +12%

* December surveys were in field between 20 December and 18 January.

**Figures are percentage balances — i.e. the difference between the % replying ‘up’ and the % replying ‘down’.

*** CBI Growth Indicator uses three-month-on-three-month growth, rather than year-on-year as used in the Distributive Trades Survey

**** Financial services are not included in the composite; the latest survey was December 2021.

Sector spotlights

Consumer, business and professional services

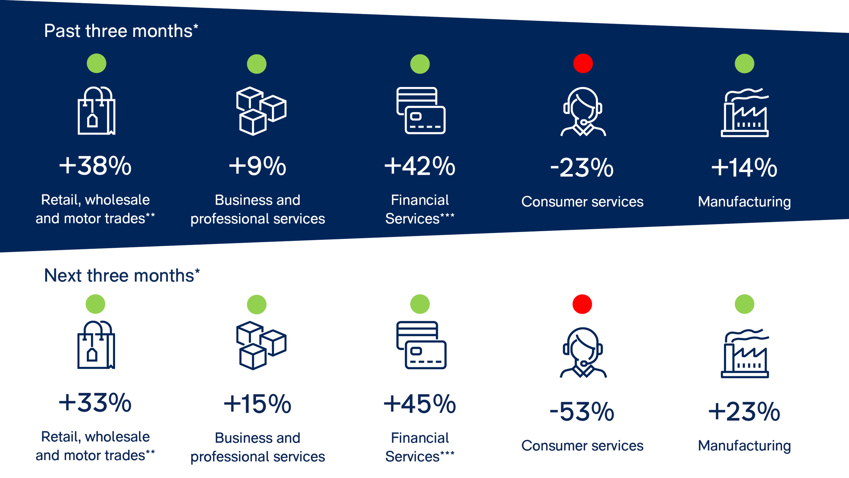

Growth in business volumes stalled across the services sector in the three months to January compared with the three months to December, reflecting a mixed performance across the two services sub-sectors. Business & professional services volumes continued to grow, albeit at a slower rate compared to the quarter to December, while consumer services volumes fell at the fastest pace since June 2021. Employment growth followed the same path, with continued growth in business & professional services headcount and a steep decline in consumer services.

The outlook for the next three months is mixed, as growth in business & professional services volumes and employment is set to accelerate, while consumer services volumes and employment are tipped to decline, with expectations the weakest in over a year for the former. Reflecting on-going cost pressures, average selling price growth is set to pick up pace in the next three months for consumer services, the strongest expectations since survey records began in July 2003. Business & professional services prices are expected to grow at a similarly strong pace to the previous quarter.

Key sector statistics:*

Business volumes (past three months):

- Total services: +2%

- Business & professional services: +9%

- Consumer services: -23%

Business volumes (next three months):

- Total services: -1%

- Business & professional services: +15%

- Consumer services: -53%

*All figures are weighted balances.

Manufacturing

Manufacturing output growth remained firm in the quarter to January, despite slowing somewhat on December. Manufacturers expect output growth to pick up next quarter. Positively, the share of firms mentioning orders or sales as a factor likely to limit output next quarter fell to its lowest since January 1974 . Total new orders in the quarter to January grew at a faster pace than in October and is expected to slow in the next quarter. In a sign that supply chain disruption remains widespread, the share of firms citing delivery dates as a factor likely to limit export orders next quarter rose to its highest since October 1974.

Numbers employed in the quarter to January increased at a slower pace compared to October, but growth remained strong by historical standards. Manufacturers expect headcount growth to pick up again next quarter. The share of firms citing skilled labour as a factor likely to limit output next quarter edged higher – to its highest since October 1973 – while concerns regarding “other” labour remained near last quarter’s record high.

Stocks of raw materials in the quarter to January grew at their quickest pace since April 2019 (when inventories rose at a record pace, just ahead of the original Brexit date), while stocks of work in progress increased at their fastest rate on record (since July 1977). By comparison, stocks of finished goods remained broadly flat.

Average cost growth quarter to January accelerated to its quickest since April 1980 and is expected to grow at a similarly fast pace next quarter. Average domestic prices in the quarter to January grew at a similarly quick rate as in October (which saw the fastest growth since April 1980), while export prices grew at their fastest pace since April 1980. Next quarter, both domestic and export price inflation is expected to pick up further.

Key sector statistics:*

- Volume of output – past three months: +14%

- Volume of output – next three months: +23%

- Total order books: +24%

- Export order books: -10%

- Finished goods stocks: -17%

- Domestic prices – next three months: +66%

*All figures are weighted balances.

Retail, wholesale and motor trades

Retail sales were seen as poor for the time of year in January, for the first time since September 2021 and to the greatest extent since March 2021. Sales are expected to remain below seasonal norms in February, albeit to a slightly lesser extent than this month.

Retail sales grew at an above average pace in the year to January, however this compares sales to January last year, when lockdowns were in force for most/all of the month (with slight variation in timings between the four UK nations). Sales are expected to grow at a slightly slower pace in the year to February. Growth in orders placed upon suppliers eased sharply in the year to January, despite being similarly impacted by base effects, but is expected to pick up next month.

Internet sales were broadly flat in the year to January for the second straight month, with expectations for flat volumes again next month.

Meanwhile, wholesalers reported sales as good for the time of year for the tenth straight month, although to a lesser extent than in December, with sales expected to be similarly above seasonal norms in February. Motor traders saw sales as good for the time of year, reversing fortunes from last month, with sales expected to be further above seasonal norms in February.

Across the distribution sector, stock volumes in relation to expected sales were seen as too low, after being broadly adequate last month, with relative stock levels seen as too low in each of the three main sectors. Stock adequacy across the distribution as a whole is expected to remain too low in February, but is expected to be broadly adequate in the wholesale sector.

Key sector statistics:*

Reported sales (year to January):

- Retail: -23%

- Wholesale: +30%

- Motor trades: +10%

Expected sales (year to February):

- Retail: -17%

- Wholesale: +30%

- Motor trades: +33%

*All figures are weighted balances.