The cost of living

The economic headlines so far this year have largely focussed on the cost of living crunch for consumers. Headline inflation rose to 5.4% in December – its highest rate in 30 years - and real wages in the year to November fell 1% (real wages were stagnant on the three-month measure).

Concerns about the increase in the energy price cap for consumers dominate the headlines and are already affecting consumer confidence. The rise in energy bills, alongside weak real earnings, particularly affects those at the lower end of the income distribution, who have also faired particularly badly during COVID-19. And this has led some to question the usefulness of the CPI as an inflation measure.

Which inflation measure matters?

Many are asking this question, but the answer is not straightforward. The CPI inflation measure is designed to capture inflation in the average household’s shopping basket.

If your spending basket is different to that of the average household, your real-world inflation experience will likewise be different. The same is true for businesses. If you’ve been experiencing double-digit rises in some of your costs for many months, it’s hard to lend much credence to an inflation measure (CPI) that has seemed so slow to respond to widely-reported inflationary pressures.

The ONS does capture an average measure of the input price inflation experienced by firms which seldom features prominently in inflation commentary. But again, it’s an average.

The growth outlook has weakened

Both consumers and businesses are set to experience elevated inflation for some time yet. In a recent note, Goldman Sachs concluded that energy prices were likely to remain elevated for another 3 years.

Meanwhile, other costs continue to rise rapidly: our latest manufacturing survey shows unit costs rising at the fastest pace in over 40 years. Alongside labour shortages and wage pressures, these pressures will remain elevated for some months, before gradually easing later in the year. They risk eroding both consumer spending and business investment this year.

The global outlook has weakened in the last few months: the IMF has downgraded its global outlook, amidst higher-than-expected global inflation, tighter COVID-19 restrictions due to Omicron, and substantial downgrades to growth in the US and China.

Going for growth

There is a role for UK governments to play in nurturing the trajectory for growth. In the short-term, easing the financial pressures on households and firms will help support growth current and next year and reduce scarring. In the longer term, we need to nurture investment and innovation, and take advantage of growth opportunities in decarbonisation.

The CBI recently called on the government to introduce a permanent investment spend tax deduction. We also called for a skills levy which is fully recycled back to businesses, supported by a new independent skills body.

We need to see longer term plans and funding structures to support the low carbon transition, and finally we need to reposition the UK globally as a competitive force through fundamental regulatory change.

Key statistics:

- Employment rate (Sep 2021 – Nov 2021): 75.5%

- Unemployment (Sep 2021 – Nov 2021): 4.1%

- Productivity growth (Output per hour, Q3 2021

vs 2019 pre-pandemic levels): +1.1% - Real wage growth (Sep 2021 – Nov 2021 on a year ago, excl. bonuses): 0.0%

- CBI growth indicator: +21%

* December surveys were in field between 22 November to 14 December (not including FSS)

**Figures are percentage balances — i.e. the difference between the % replying ‘up’ and the % replying ‘down’.

*** CBI Growth Indicator uses three-month-on-three-month growth, rather than year-on-year as used in the Distributive Trades Survey

**** Financial services are not included in the growth indicator composite; the latest FSS was December 2021.

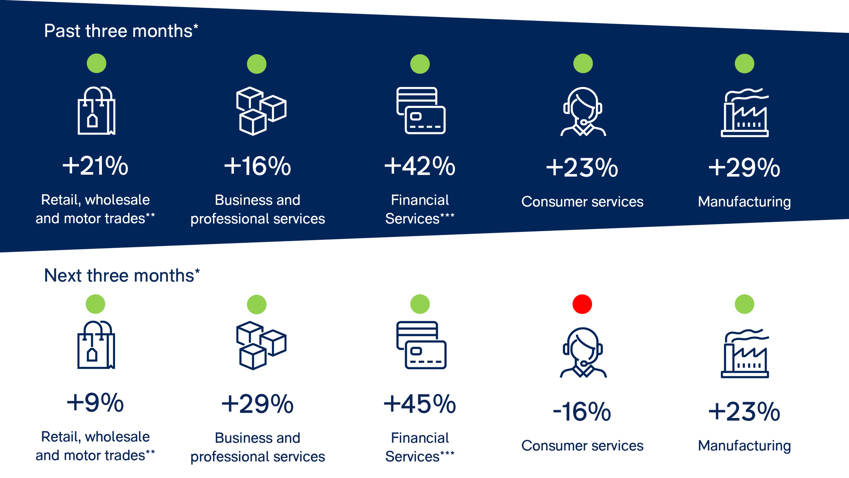

Sector spotlights

Consumer, business and professional services

Business volumes across the services sector grew at a much slower, albeit still solid, pace in the three months to December compared with the same period one month previously. Both business & professional services and consumer services saw a slower rate of growth compared to last month, although the decline was much more pronounced in the former. Employment growth amongst business & professional services firms also slowed, though headcounts nevertheless increased. Consumer services employment remained unchanged in the quarter to December, after growing last month.

The outlook for the next three months is mixed, as growth in business & professional services volumes is set to accelerate, while consumer services volumes are tipped to decline at pace. It is worth noting that around a third of survey responses came in before the announcement of plan B measures on the 8th December (our December field period ran to 14th December). Employment is expected to see strong growth in the quarter ahead. Average selling price growth is set to pick up pace in the next three months, the strongest expectations since survey records began in July 2003.

Key sector statistics:*

Business volumes (past three months):

- Total services: +18%

- Business & professional services: +16%

- Consumer services: +23%

Business volumes (next three months):

- Total services: +18%

- Business & professional services: +29%

- Consumer services: -16%

*All figures are weighted balances.

Manufacturing

Manufacturing activity strengthened in December, despite ongoing supply challenges. Output volumes in the quarter to December grew at their fastest pace since July 2021, reflecting broad-based growth across sub-sectors.

Manufacturers expect output growth to slow moderately (but remain quick by historical standards) next quarter. Total order books in December were judged to be “above normal” to a similar extent to last month’s record-high, while export orders were reported as broadly “normal”.

Manufacturers’ inventory positions deteriorated further in December, with stock adequacy of finished goods worsening to a new record-low position for the second month in a row. Price pressures are anticipated to remain acute in the next three months.

Key sector statistics:*

- Volume of output – past three months: +29%

- Volume of output – next three months: +23%

- Total order books: +24%

- Export order books: -1%

- Finished goods stocks: -24%

- Domestic prices – next three months: +62%

*All figures are weighted balances.

Retail, wholesale and motor trades

Retail sales grew in the year to December at a much slower rate than last month, disappointing expectations for an acceleration in growth. Both reported and expected sales growth deteriorated throughout the survey field period for both retail and distribution as a whole as concerns about Omicron increased (our December survey field period ran to 14th December, with plan B announced on the 8th ).

Sales are expected to grow at a similarly below-average pace next month. Internet sales were broadly flat in the year to December but are expected to fall next month, although this will partly be impacted by base effects around last year’s winter lockdown and the timing of black Friday sales, and the bringing forward of sales this year to November due to concerns around stock shortages. Sales were seen as broadly average for the time of year in December and are expected to be poor for the time of year next month.

Orders placed upon suppliers grew at a faster pace than November, while stock levels in relation to expected sales recorded a positive balance for the first time since February. Anecdotes from respondents indicate that many distribution firms are looking to hold higher than usual stock levels in order to combat ongoing supply chain disruptions, including ordering larger quantities and ordering further in advance. Orders growth is expected to slow next month, with relative stocks expected to be broadly adequate.

Elsewhere, wholesalers reported slowing sales growth in the year to December and expect a similar rate of growth next month. Motor traders reported sales as falling in the year to December and expect sales to decline next month also.

Key sector statistics:*

Reported sales (year to December):

- Retail: +8%

- Wholesale: +27%

- Motor trades: -18%

Expected sales (year to January):

- Retail: +5%

- Wholesale: +27%

- Motor trades: -12%

*All figures are weighted balances.

Financial services

Financial services growth picked up in the quarter to December, reflecting a strong period of activity ahead of the imposition of Plan B restrictions in England (the survey was in the field from 22 November to 10 December). Business volumes growth accelerated to its fastest pace since June 2017, which contributed to a speeding up in profitability growth (to its quickest since December 2015). The value of non-performing loans declined at a slightly slower rate compared to last quarter, and numbers employed were unchanged for the second quarter in a row. Sentiment in December rose for the sixth quarter in a row, but at a slower pace than in September.

Looking ahead to the next quarter, FS firms expect activity to remain robust. Business volumes in the next quarter are expected to grow at a similarly strong pace. The value of non-performing loans is anticipated to be flat, while profitability growth is expected to ease. Headcounts are set to grow next quarter. Firms expect investment in IT to grow over the next year (relative to this past year), but to a lesser extent than last quarter.

Investment in IT is expected to grow in the next 12 months (relative to the past 12), but to a lesser extent than last quarter. Meanwhile, investment intentions deteriorated for land & buildings and vehicles, plant & machinery. The most common factor cited as likely to limit investment over the next 12 months was uncertainty about demand, though concern over labour shortages rose considerably further above its long-run average.

Key sector statistics:*

For past three months:

- Business volume: +42%

- Overall profitability: +42%

- Numbers employed: 0%

For next three months:

- Volume of business: +45%

- Overall profitability: +30%

- Numbers employed: +21%

*All figures are weighted balances.