GDP to see a one-off fall over Q2

Business surveys are pointing to a weakening in economic activity, with both the CBI’s Growth Indicator and the Purchasing Managers’ Index (PMI) indicating a sharp slowing in growth over the last couple of months. This follows already sluggish GDP data: excluding drags from Test & Trace and COVID vaccination activity unwinding, official data shows that economic momentum remained tepid going into Q2. Alongside softer business surveys and the extra bank holiday in June, this means that the economy is likely to contract over the quarter (our own forecast is for GDP to decline by 0.2%). However, this is unlikely to mark the start of a recession – with Q3 having a full set of working days, activity should rebound (we expect growth of 0.4%).

Inflation continues to rise

But looking through this near-term volatility, it’s clear that we’re set for a period of weaker economic growth ahead. The principal driver is high inflation, and the subsequent squeeze on households’ real incomes and spending. CPI inflation rose to 9.1% in May, remaining at a 40-year high. Strong price rises are becoming more broad-based: of the 86 individual items in the CPI basket, around half saw inflation of 7% or above.

Near-term risks to inflation are to the upside. The May CPI data was collected before domestic fuel prices rose again, suggesting that this will show up in the June data. Global oil prices have risen further, and the strength in wholesale energy prices has led to speculation of another large rise in Ofgem’s energy price cap in October, to a greater degree than analysts were already predicting. The pound has also fallen in recent weeks, which raises the cost of imported goods.

But further ahead, inflation risks can either be categorised as more balanced or slightly to the downside. A weakening in economic growth and households’ purchasing power should take some of the heat out of price rises. There are already some tentative signs of this: while headline CPI inflation rose in May, “core” inflation (i.e. excluding food and energy) fell back a touch (to 5.9%), for the first time in eight months.

Labour market tightness cement the case for more rate rises

But for now at least, consumer price inflation is likely to remain high over the year ahead. This puts the Bank of England in an tricky bind, given the need to calibrate monetary policy to both reign in inflation, and avoid choking off growth. The Monetary Policy Committee (MPC) seem to be prioritising the former objective for now, and voted to raise interest rates again in June – the fifth successive rise, bringing Bank rate to 1.25%. Three members of the Committee voted to raise rates even further (to 1.5%), and minutes of their meeting stressed that the MPC would act “forcefully” if inflationary pressures prove to be more persistent.

A key factor swaying the MPC towards further rate rises is the tightness in the labour market, and the subsequent threat that high inflation could feed through to pay awards. There is little sign of this occurring so far: both pay surveys and data on pay settlements remain contained (though anecdote suggests that pay awards are much higher for specific roles). But it’s clear that developments in the labour market – particularly against the backdrop of weaker economic growth ahead – is something that the MPC will be keeping a close eye on during their future deliberations.

Key statistics:

- Employment rate (February 2022 – April 2022): 75.6%

- Unemployment (February 2022 – April 2022): 3.8%

- Productivity growth (Output per hour, Q1 2022

vs 2019 pre-pandemic levels): +1.5% - Real wage growth (February 2022 – April 2022 on a year ago, excl. bonuses): -2.2%

- CBI growth indicator: +5%

*June surveys were in field between 25 May and 14 June (not including FSS).

**Figures are percentage balances — i.e. the difference between the % replying ‘up’ and the % replying ‘down’.

*** CBI Growth Indicator uses three-month-on-three-month growth, rather than year-on-year as used in the Distributive Trades Survey

**** Financial services are not included in the growth indicator composite; the latest FSS was March 2022.

Sector spotlights

Consumer, business and professional services

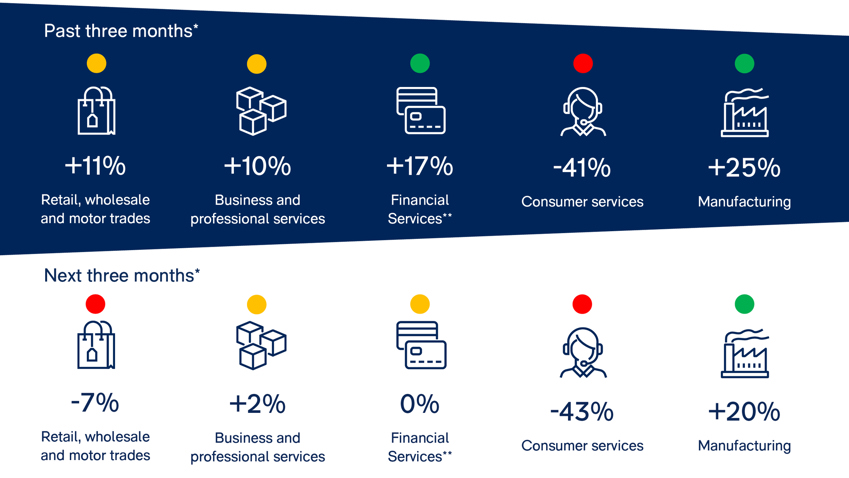

Business volumes growth stalled in the service sector as a whole in the three months to June. Services sub-sectors saw a divergence in conditions, with business and professional services volumes continuing to grow but at a slower pace than the previous month, while consumer services volumes dropped sharply over the last three months, at the fastest pace since February 2021. Employment growth in business & professional services eased over the last quarter, compared to a drop in headcount in consumer services.

Next quarter, volumes in business & professional services are expected to be broadly unchanged, with a slight acceleration in employment growth expected. In contrast, consumer services volumes are set to fall at a similar pace while employment is expected to fall at a slightly faster rate. Given growing cost pressures across the economy, expectations for average selling prices growth remain elevated for the next three months for both consumer services and business & professional services.

Key sector statistics:*

Business volumes (past three months):

- Total services: -2%

- Business & professional services: +10%

- Consumer services: -41%

Business volumes (next three months):

- Total services: -9%

- Business & professional services: +2%

- Consumer services: -43%

*All figures are weighted balances.

Manufacturing

Growth in output volumes slowed in the three months to June, while total order books and export order books also softened. Stocks of finished goods were seen as adequate, having been inadequate for much of the past year. Output growth is expected to ease further in the quarter ahead, while expectations for domestic price growth in the next three months fell back to a nine-month low.

Key sector statistics:*

- Volume of output – past three months: +25%

- Volume of output – next three months: +20%

- Total order books: +18%

- Export order books: +1%

- Finished goods stocks: +2%

- Domestic prices – next three months: +58%

*All figures are weighted balances.

Retail, wholesale and motor trades

Retail sales volumes fell slightly in the year to June, marking the third successive month in which volumes have failed to grow. Sales were seen as poor for the time of year in June. The volume of stocks in relation to expected demand was seen as too high for a second consecutive month (although stock adequacy nonetheless remains below its long-run average, having fallen during the pandemic). With sales volumes slipping back in the year to June, retailers also reported lower orders with suppliers—a fourth consecutive month of flat or falling orders.

Looking ahead, retailers expect sales volumes to be flat over the year to July and to remain well below seasonal norms. Stocks are expected to remain too high, while orders are expected to decline at a broadly similar rate as in the year to June.

Key sector statistics:*

Reported sales (year to June):

- Retail: -19%

- Wholesale: +20%

- Motor trades: +32%

Expected sales (year to July):

- Retail: -25%

- Wholesale: +12%

- Motor trades: +10%

*All figures are weighted balances.