Business resumes

The sad passing of HM the Queen led to a pause in parliamentary business. But while the UK has been in formal mourning, economic conditions have continued to be torrid. The appointment of a new prime minister unleashed a flurry of announcements to address the impact of soaring energy bills on consumers and businesses. But businesses have been left hanging regarding the detail of the business package and the affordability of a mammoth £150 billion stimulus package. Meanwhile, the pound hit another 37 year low against the dollar following disappointing retail sales data, the latest labour market data saw the biggest quarterly rise in inactivity since the pandemic began, and rising underlying inflation is putting pressure on the MPC to deliver a 75 basis point rise in rates.

The outlook for the UK economy

The UK’s economic outlook has jumped around considerably over the past couple of months. In June, the CBI’s forecast was for 2023 growth of 1% and average inflation of 4.1%. After political interference in pipeline gas supply to Europe in early July, the Bank’s August forecast was for 2023 growth of -1.5% and inflation of 9.6%. The UK government’s price cap announcement in September then led to another shift in forecasts, with latest estimates for GDP growth in 2023 at around 0, and inflation around 5%.

The composition and scale of the Truss fiscal package will be important for refining economic forecasts further and for later years. As well as beneficial effects on the level of inflation and growth which are an arithmetic function of the price cap, there will be business and consumer confidence impacts too. Most significant though will be the Bank of England’s interest rate response. Interest rates are rising in part because demand is outpacing supply. A fiscal injection pours fuel on that fire, meaning interest rates will rise further and faster, tightening finance conditions for businesses and households. The UK is buffeted by many of the same storms affecting continental Europe, particularly energy and other commodity price volatility and post pandemic supply chain disruption.

UK labour market no longer gives competitive edge

Sterling has had a volatile summer, amidst ever worsening economic data. The euro hasn’t had an easy ride either, likewise approaching parity with the dollar. But while the UK shares Europe’s exposure to Russian manipulation of gas prices, the labour market is where the UK appears a global outlier. Both the Eurozone and US have labour market activity back at pre-pandemic levels, but the UK’s active population (the number of people in employment or actively seeking work), has recently seen most of its post-pandemic recovery unwind.

It’s no surprise that recruitment challenges remain one of the top issues on CBI members’ minds: the number of unemployed people per vacancy is the lowest on record; wage growth is rising; and employers are having to get ever-more creative in sourcing talent. The extent to which UK inactivity reflects a significant worsening in the performance of the health service is of increasing concern: another issue to add to the significant task list of the new cabinet.

Key statistics:

- Employment rate (May 2022 – July 2022): 75.4%

- Unemployment (May 2022 – July 2022): 3.6%

- Productivity growth (Output per hour, Q2 2022

on a year ago) -1.0% - Real wage growth (May 2022 – July 2022 on a year ago, excl. bonuses): -2.8%

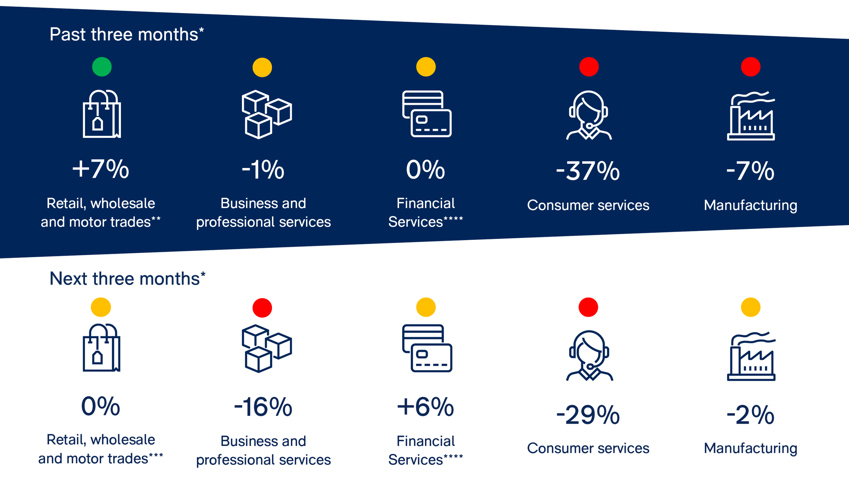

- CBI growth indicator: -5%

* August surveys were in field between 26 July and 15 August. (not including FSS).

** Figures are percentage balances - i.e. the difference between the % replying ‘up’ and the % replying ‘down’.

*** CBI Growth Indicator uses three-month-on-three-month growth, rather than year-on-year as used in the Distributive Trades Survey

**** Financial services are not included in the growth indicator composite; the latest FSS was June 2022.