A chilly outlook for the UK economy

The CBI published its latest forecasts for the UK and global economies on 5 December. We’re predicting that there’ll be a shallow recession over the coming year, with a peak to trough decline in output of 0.7%, rather smaller than the OBR’s 2% decline and considerably smaller than the financial crisis recession (peak-to-trough output decline of 6.3%). Our forecast is less bad than the OBR’s in part because, unlike the OBR, we have more freedom to use our own expectations for interest rates, and have rates peaking at 4% next year, rather than the 5% in the OBR’s model.

In the absence of further shocks, we expect consumer inflation to fall rapidly to around 4% at the end of 2023. In 2024, we expect growth of 1.6%, as the squeeze on consumer incomes abates and inflation continues to fall back. But business investment suffers in our forecast from the expiration of the super deduction, higher financing and other costs, labour shortages, a weaker housing market and a weak economy. Unfortunately, this underpins an even weaker outlook for UK productivity and potential growth, and ultimately for living standards. With the global economy expected to weaken next year too, there’s little support coming through from trade.

Forecast uncertainty

Any forecast is inherently uncertain. But with economies reeling from the effects of the pandemic on supply chains and labour markets, and the addition of a European war, predictions are more uncertain than usual. Our forecast is predicated on the market path for energy. But there is considerable uncertainty regarding the outlook for energy supply in Europe as we transition away from Russian supplies in the near-term and shift to renewable energy sources.

Then there’s the labour market in the UK, which has suffered the loss of over 900,000 since the pandemic, 40% of whom are over 65 and so may never return, and 28% of whom are long-term sick. Analysis is being conducted to try and understand the nature of inactivity in the UK, in conjunction with recent trends in migration, to refine the mix of policy solutions which can improve the availability of people across the skill spectrum. In the meantime, we expect that some people will return to the labour market over the next couple of years as cost of living pressures bite and erode savings amassed during the pandemic, and we expect demand for labour to ease as the economy slows, such that the unemployment rate rises to 5% from its current 3.6% level.

The next fiscal event

The Autumn Budget reinforced the UK’s macroeconomic stability, which was absolutely crucial. But with a grim economic outlook, the UK desperately needs a plan for growth. It’s welcome that clarification of future support on energy costs for business is looking likely to be announced soon. But businesses are facing a plethora of headwinds, in the near-term, and the prospect of higher taxes further out. We are facing into a protracted squeeze in household incomes and business margins. Providing the right tax, regulatory and financial frameworks to support business in delivering the investment needed to lift UK productivity and living standards, and accelerate the net-zero transition, is more necessary than ever.

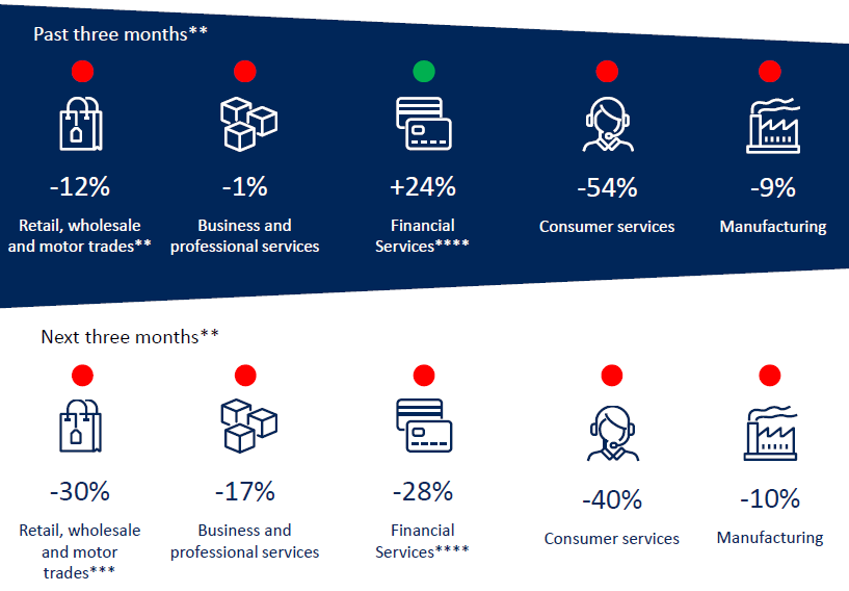

The picture in key sectors of the UK economy

* November surveys were in field between 26 October and 15 November (not including FSS).

**Figures are percentage balances — i.e. the difference between the % replying ‘up’ and the % replying ‘down’.

*** CBI Growth Indicator uses three-month-on-three-month growth, rather than year-on-year as used in the Distributive Trades Survey.

**** Financial services are not included in the growth indicator composite; the latest FSS was September 2022.

Colour indicators illustrate whether the reported balance is above (green), below (red), or close to (orange) the long run average.