Bank of England upgrades outlook

The Bank’s forecast for growth this year is now in line with the CBI’s December forecast for a mild decline in activity this year. Market expectations for interest rates have shifted down since the mini-Budget and activity data for the UK so far this year has been a little better than expected.

The Bank now expects that the economy grew marginally over the last few months of 2022. It also seems more confident that headline inflation has passed its peak, highlighting easing supply chain disruption and falling gas prices. But the Bank also notes that domestic inflationary pressures are “firmer than expected” – particularly wage growth and inflation in the services economy. Overall, the Bank seem marginally less concerned about inflation becoming entrenched. Gone from the rhetoric is the pledge to “respond forcefully” to signs of persistent inflationary pressures, with the MPC saying “further tightening in monetary policy would be required” if such pressures materialise. All in all, a welcome (mild) improvement in tone from the Bank.

IMF highlights the headwinds facing the UK

In the same week as the Bank of England’s latest interest rate decision and monetary policy report, we’ve had interest rate decisions by both the Fed and the ECB. As trailed at Davos, the IMF upgraded its forecasts for advanced economies with the notable exception of the UK, which received a hefty downgrade. It is most definitely worth noting that this downgrade only brings its forecast in line with both the Bank and CBI forecasts for the UK this year. But the UK still stands out as the only advanced economy forecast to be in recession in 2023.

The IMF cites many headwinds to UK growth: tighter fiscal and monetary policies; high energy prices (despite recent falls); a tight labour market (like the US); strong underlying inflation; less generous government support for energy bills than other European countries; ongoing trade frictions as the UK continues to negotiate its trading relationship with the EU; and lingering fall-out from the market reaction to the mini-Budget. Quite the list of challenges…

The run-up to the Budget: four pillars and a five-point plan

The New Year saw a five-point plan from the Prime Minister: to halve inflation by the end of the year (which we and the Bank judge that he’ll achieve); to grow the economy (a bit harder); to get national debt falling (which was clarified as sticking to existing plans); falling NHS waiting lists (hard); and stopping small boats (hard). The Chancellor has now added a helpfully alliterative list of four pillars: enterprise, education, employment, and everywhere - a tad W1A, but definitely the right themes. He has described the sort of policies that could be helpful, repeating much of the Autumn Budget. But there were some hints to the direction of future policy: In particular, aiming for the most competitive tax regime of any major country and making work worthwhile for the over 50s.

In our latest Budget submission, we reiterate our desire for a successor to the super deduction and propose solutions to labour market shortages. But although the economy is brighter, the finances are tight. The Chancellor will need to strike the right balance between macroeconomic stability and well-targetted policy to support the UK’s potential, particularly on innovation and the green economy.

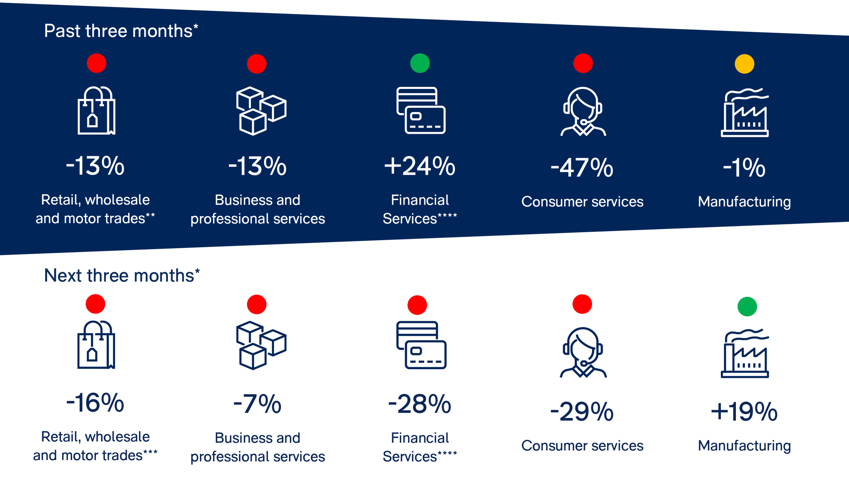

The picture in key sectors of the UK economy

* January surveys were in field between 19 December and 13 January.

**Figures are percentage balances — i.e. the difference between the % replying ‘up’ and the % replying ‘down’.

*** CBI Growth Indicator uses three-month-on-three-month growth, rather than year-on-year as used in the Distributive Trades Survey.

**** Financial services are not included in the growth indicator composite; the latest FSS was December 2022.

Colour indicators illustrate whether the reported balance is above (green), below (red), or close to (orange) the long run average.