The economy this year

The new year has kicked off with the usual reflections by learned commentators on where economies are headed. Global growth in 2023 is actually expected to be fairly similar to 2022, but the Eurozone, the US and the UK are all likely to see growth slip. All three regions will see ongoing high inflation continue to erode consumer spending, while higher interest rates will increasingly feed through to increased mortgage payments and weaker housing markets. Monetary policy will tighten further this year before steadying as the impact of higher interest rates on household and businesses’ spending decisions deepens.

Labour markets are relatively tight across all three regions, but demand for labour is expected to fall over the year as overall demand weakens, leading to higher unemployment and a gradual softening in wage settlements. Europe and the UK have a greater energy challenge than the US, given their proximity to Russia and the separation of global gas markets. The intensity of the UK’s challenges is heightened by concerns that ill health is affecting the economy and labour market, as well as building evidence that the UK’s current trading relationship with Europe is exerting a heavy toll on UK trade and the economy.

Structural themes for 2023

The global economy faces a heady mix of cyclical challenges this year. But there are plenty of other themes to keep boardrooms busy in the months ahead. A focus on sustainable energy supply will remain a priority this year for policy-makers and businesses, as the switch-away from Russian oil and gas continues and the transition to green energy accelerates. Another important area to keep an eye on will be the stability of global financial systems as the west transitions from low interest rates for the first time in 15 years. And geopolitics will continue to be a running theme with the Ukraine war, China’s post-zero Covid policy shake-out and the impact of the Inflation Reduction Act on the US-EU relationship jockeying for position.

The role of cryptocurrencies will continue to evolve, after a few bruising months for crypto investors, with regulators very clearly setting out their desire/intent to bring them into their purview. Although the tech sector has had a rough year, with key stocks down some 30%, tech adoption and exploitation will continue to be a priority for firms. The impressive performance of ChatbotGPT has really highlighted how advanced AI has become, and demonstrates the huge implications that such technology could have for companies and individuals.

The Prime Minister sets out his stall

The PM was quick off the mark in launching his new year brand refresh, built around five pledges: to halve inflation, grow the economy, reduce government debt, cut waiting lists and stop small boats. For the CBI, an ambition to grow the economy is very much a priority we share, and in the coming weeks, we’ll be putting out our Budget submission ahead of Chancellor Hunt’s Budget speech on 15 March. That speech will be accompanied by a fuller OBR report than we received in Autumn (with that report hamstrung by repeated Autumn Budget date changes). Ahead of that, we’ll have a Monetary Policy Report and interest rate decision by the Bank of England on 2 February. Happy New Year!

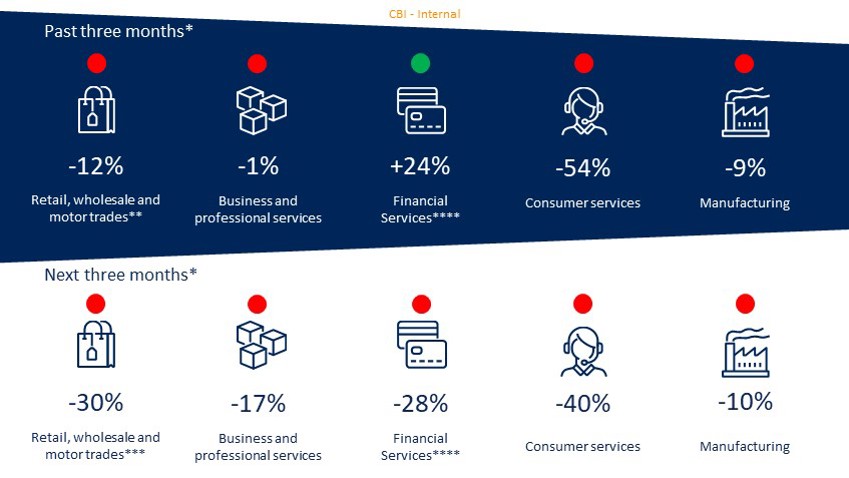

The picture in key sectors of the UK economy

* December surveys were in field between 23 November and 13 December.

**Figures are percentage balances — i.e. the difference between the % replying ‘up’ and the % replying ‘down’.

*** CBI Growth Indicator uses three-month-on-three-month growth, rather than year-on-year as used in the Distributive Trades Survey.

**** Financial services are not included in the growth indicator composite; the latest FSS was December 2022.

Colour indicators illustrate whether the reported balance is above (green), below (red), or close to (orange) the long run average.