What a week…

The government’s fiscal package certainly landed with a bang, but not in quite the way they were hoping. Trussonomics proved too big for markets to swallow, in the context of gas pipeline interventions by Russia and swiftly rising interest rates globally. The government’s plan amounted to additional borrowing of £80bn in 2022-23 alone (£60bn of which is the energy package), with longer term additional borrowing of £45bn per year. The longer term cost is largely driven by NI, income tax and corporation tax – the recent u-turn on the 45p income tax rate saves only £2bn.

In the short-term, substantial tax cuts provide a boost to the economy, but experience to-date has not shown these kinds of tax cuts to be effective in enhancing the economy’s capacity to grow without generating inflation. Meanwhile, the supply side reforms announced – while welcome – do not appear sufficient to meaningfully enhance growth either. And in the context of consumer inflation of around 10%, it risks monetary and fiscal policy acting in opposition to one another. We look forward to the OBR’s assessment of the package (and indeed the Bank of England’s – they’ll be publishing new forecasts on 3 November) with bated breath.

Current economic conditions

Behind the political noise, economic momentum is already slowing. Although the ONS recently published revisions to UK GDP that showed that the economy had in fact grown in Q2 (by 0.2% against a first estimate of -0.1%), our recent surveys show activity falling across-the-board in Q3, and expectations for faster falls in Q4. Consumer confidence reached a new record low in September, following disappointing retail sales data in August. Sharply rising energy prices from July (relating to disrupted gas supplies in Europe) are likely to have affected business and consumer confidence alike over the summer. Meanwhile, the UK’s labour market has got tighter, with the latest official data showing that inactivity rose sharply (by 154,000) in the quarter to July.

Although there are early signs that some costs are rising less swiftly – the prices of raw materials and fuel (input prices) were up 20.5% on the year to August, below their peak of 22.6% in July – market interest rates are now higher, putting pressure on businesses and households borrowing on variable rates in particular. And while sterling has recovered its losses over the past couple of weeks (at least, at the time of writing), it has depreciated 8% over the year against a trade-weighted basket of currencies, adding further to costs.

What next?

The economic outlook depends heavily upon fiscal and monetary policy. In the short-term, looking through the political noise, the energy support package is expected to alleviated the worst of the energy crisis for households and businesses, softening the extent of the downturn. It seems reasonable to expect that the OBR will be allowed to pass judgement on the overall sustainability of the fiscal package that makes it to the next Budget event. But given the commitment to fiscal sustainability made by the government, we will likely see spending cuts. As for interest rates, markets should settle, but an unusual fiscal gamble by the UK has made the UK a less safe bet, and the price is higher interest rates.

Key statistics:

- Employment rate (May 2022 – July 2022): 75.4%

- Unemployment (May 2022 – July 2022): 3.6%

- Productivity growth (Output per hour, Q2 2022

on a year ago) -1.0% - Real wage growth (May 2022 – July 2022 on a year ago, excl. bonuses): -2.8%

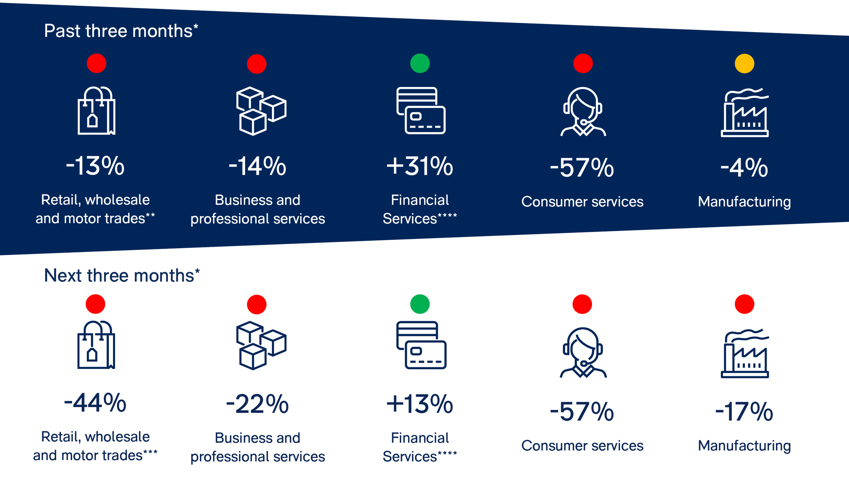

- CBI growth indicator: -19%

* August surveys were in field between 26 July and 15 August. (not including FSS).

** Figures are percentage balances - i.e. the difference between the % replying ‘up’ and the % replying ‘down’.

*** CBI Growth Indicator uses three-month-on-three-month growth, rather than year-on-year as used in the Distributive Trades Survey

**** Financial services are not included in the growth indicator composite; the latest FSS was June 2022.